Our housing availability and affordability problem is having perverse effects on work, intergenerational mobility, entrepreneurship, fertility and family formation.

When I recently caught up with an old Labor friend from university, our discussion turned to why some Millennials and Gen Zs apparently show less interest than previous generations to work extra hard to advance their careers.

My friend offered an insightful answer. Homes have become unaffordable for many people aged in their 20s and 30s, so what’s the point in slaving away at the office and dedicating extra hours if it won’t allow you to scrape together a home deposit?

The obvious fix is fast-tracking supply, supply and more supply of homes in inner and middle-ring neighbourhoods close to good jobs and existing infrastructure. Fairfax

Our housing availability and affordability problem is likely having perverse effects on work incentives, intergenerational mobility, entrepreneurship, fertility and family formation.

It is arguably the No.1 combined economic and social issue facing the nation.

The obvious fix is fast-tracking supply, supply and more supply of homes in inner and middle-ring neighbourhoods close to good jobs and existing infrastructure – as NSW is pledging to do.

null

Advertisement

Nationally, new house approvals have fallen to their lowest level in nearly 12 years, the Australian Bureau of Statistics said on Monday.

The Albanese government has dangled $3 billion to states to streamline the building of 1.2 million homes over five years. But the current building slump, exacerbated by red tape for zoning and planning, high interest rates and expensive building costs, suggests governments will fail.

Australians need a more serious effort from the Commonwealth, states and local governments to enable the construction of more homes.

There are too many pretend policies that fail to deal with the magnitude of the problem.

The Greens have a whacky idea to establish a government property developer.

The Albanese government’s Housing Australia Future Fund for social and affordable housing and shared equity scheme for 10,000 annual low-deposit buyers are a drop in the ocean compared with what the private sector needs to deliver.

Peter Dutton launched a populist attack on the sensible idea to rezone inner-city defence land for housing. The Liberals want to allow first home buyers to tap superannuation for housing, which will push up prices unless there is a massive increase in housing supply.

Negative gearing and capital gains tax in the firing line

The Greens have a whacky idea to establish a government property developer and want to crack down on negative gearing and the 50 per cent capital gains tax (CGT) discount.

It’s not surprising Australians leverage into property and punt on capital gains. Australia has relies heavily on personal income tax with the top 47 per cent rate kicking in at an internationally modest threshold of $180,000.

Punishing wage-earning taxpayers entices them to turn to the property market to reduce their income tax bill and bet on capital appreciation.

Do the Greens realise their opposition to the stage three income tax cuts makes negative gearing more attractive?

Tax should be part of the conversation about housing. But it is not a panacea.

The zero-tax on the principal place of residence and exclusion of the family home from the asset test for the government age pension are putting upward pressure on home prices by encouraging over capitalisation. But they are considered politically untouchable.

Replacing stamp duty – such as with land tax or a higher GST – on property purchases would remove a barrier to moving. It would enable a better allocation of large and small homes between growing families and empty nesters, and also improve labour mobility by making it easier to move closer to jobs.

Centre for Independent Studies chief economist Peter Tulip says a range of research by left and right-wing institutions estimates that negative gearing and the CGT discount add only about 1 per cent to 4 per cent to house prices.

Investors, like businesses, are entitled to claim a deduction for interest and other expenses incurred to provide housing. It is a basic principle of tax policy and law.

Nevertheless, the 50 per cent CGT discount is worthwhile scrutinising because of its interaction with negative gearing.

The only reason running an investment property at an annual loss can make financial sense is future capital gains, a strategy made more attractive by the discount.

Investors can defer CGT paid on home sales to when the time is right, such as retirement when they have minimal other taxable income and face lower marginal tax rates.

During their younger and higher earning years when their marginal tax rates are high, they claim mortgage interest deductions against wages.

The 50 per cent discount on nominal capital gains replaced the inflation-indexed taxation of real capital gains from September 1999 under the Howard government.

The concession was introduced on all investable assets such as shares – not just houses – held longer than 12 months. It was in response to the Ralph review of business taxation and was intended to motivate entrepreneurship and risk-taking by small business.

Instead, it triggered a surge in mum and dad property investors. Existing housing is a relatively unproductive asset, so arguably it doesn’t deserve as large a CGT discount.

Yet, even if the 50 per cent CGT discount was made less generous, there would need to be some sort of concession to ensure only inflation-adjusted real gains are taxed (like pre-1999), or a smaller CGT discount is applied to nominal gains (Labor proposed a 25 per cent discount at the 2019 election).

Tilting the tax system away from investors might slightly increase homeownership rates as owner-occupiers replace some would-be investors.

But fewer tax incentives for investors would not boost housing supply and, if anything, could reduce the building of homes and put some modest upward pressure on rents.

If governments want more homes built, they first need to reduce the size of their massive infrastructure pipeline, particularly “Victoria’s big build”, which is poaching tradies and cement trucks and inflating construction material costs for home builders.

Financial incentives for councils

Instead of the Albanese government paying financial incentives to states, a better approach may be to offer some of the payments directly to councils to achieve home-building targets.

It is often councils that control the planning and zoning red tape stalling the construction of houses and apartments.

Tied Commonwealth grants to councils could be paid if home-building completion targets are achieved. Councils could be required to pass the money to residents, either through cheaper rates and/or investment in community infrastructure.

The NIMBY resistance could be less potent if incumbent homeowners permitting higher density homes in their neighbourhoods saw a direct financial benefit on their rates bills.

Moreover, residents worried about losing sunlight and more cars on their streets often don’t realise they financially benefit from upzoning to allow more medium and high density homes.

The value of their land increases because of the opportunity to develop multiple homes on it. But the price of each smaller home is cheaper for buyers than a single-home on a block.

It is perhaps one of the very few economic “free lunches” available.

The NSW Minns Labor government is making the right political noises on supply and density.

If it succeeds in crashing through NIMBYism, it would be a big economic and social reform rivalling some of the feats of the Hawke-Keating Labor government.

One of the blockages Labor will need to overcome in the NSW planning system is the overly bureaucratic Sydney Water and Ausgrid, which delay developments approvals and subdivisions for many months.

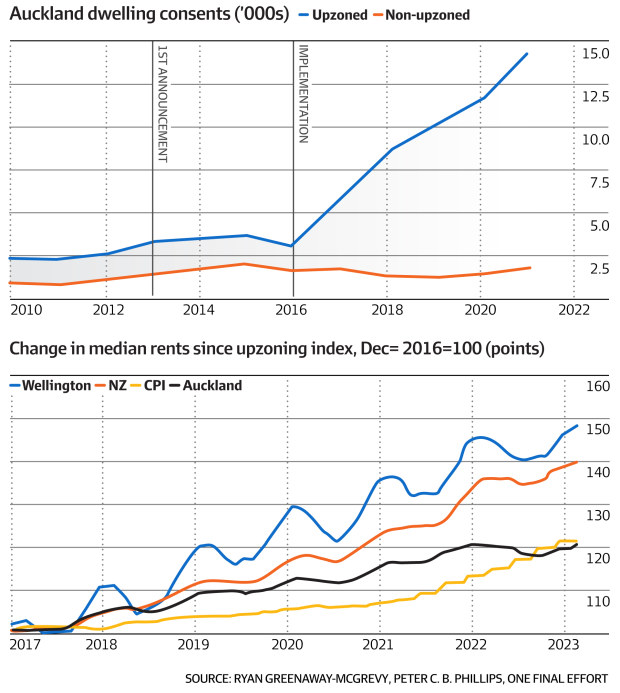

New Zealand offers a way forward

New Zealand’s experience shows when housing supply and density are significantly boosted, prices and rents become relatively cheaper.

A radical move to liberalise zoning laws in Auckland helped fuel a building boom that has spared the region from the big increase in house prices and rents across the rest of the country.

Since 2016, rents have increased 10 per cent to 20 per cent in Auckland, compared with about 40 per cent in Wellington. House prices are about 20 per cent higher, compared with the 70 per cent lift that occurred outside Auckland.

If governments can emulate the Kiwis, more Australians will have a hope of affording to own or rent a home.

John Kehoe is Economics editor at Parliament House, Canberra. He writes on economics, politics and business. John was Washington correspondent covering Donald Trump’s election. He joined the Financial Review in 2008 from Treasury. Connect with John on Twitter. Email John at jkehoe@afr.com

New Malaysia Herald publishes articles, comments and posts from various contributors. We always welcome new content and write up. If you would like to contribute please contact us at : editor@newmalaysiaherald.com

Facebook Comments

Facebook Comments